Why Starting SIP at 30 Beats 40: ₹5 Crore Retirement Plan

Building a substantial retirement corpus by 40 requires smart planning and consistent action. The journey to financial independence starts with understanding one crucial principle: time is your greatest asset. Investing in a ₹5 Crore Retirement Fund can significantly enhance your financial security.

Why Starting Early Matters

When you delay investing, you miss out on compound growth—the process where your returns generate additional returns. While the impact might not seem obvious initially, the difference becomes dramatic over decades.

Additionally, planning for a ₹5 Crore Retirement Fund early can provide peace of mind as you approach retirement, allowing more time for your investments to grow.

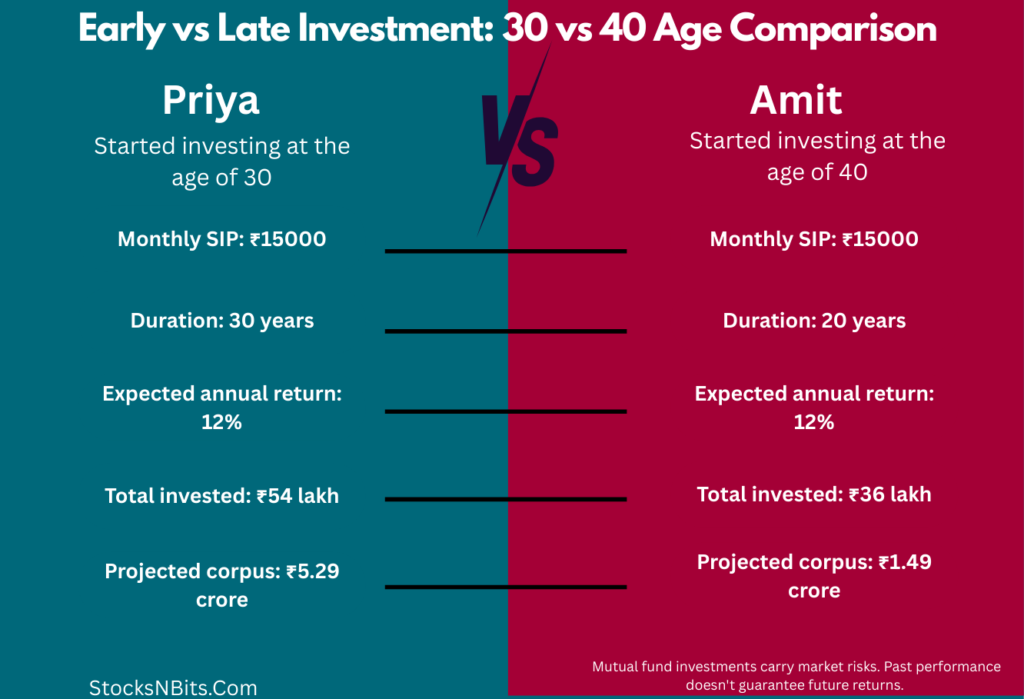

Consider this scenario: Priya begins investing at 30, while Amit waits until 40. Both invest the same monthly amount until they turn 60. The gap in their final corpus? It’s substantial enough to change retirement plans completely.

Mutual Funds for Long-Term Wealth Creation

Equity mutual funds offer an accessible path to building wealth without requiring deep market expertise. Unlike direct stock investing, professional fund managers handle asset allocation based on the scheme’s objectives. You can start with as little as ₹500 monthly through Systematic Investment Plans (SIPs), making wealth creation achievable for regular earners.

SIPs work particularly well for those who prefer steady monthly contributions over large one-time investments.

Real Numbers: The Cost of Waiting

Let’s examine how timing affects wealth accumulation with a ₹5 crore target:

Scenario 1: Starting at Age 30 (Priya)

-

Monthly SIP: ₹15000 -

Duration: 30 years -

Expected annual return: 12% -

Total invested: ₹54 lakh -

Estimated Return: ₹4.75 crore -

Projected corpus: ₹5.29 crore

Scenario 2: Starting at Age 40 (Amit)

-

Monthly SIP: ₹15,000 -

Duration: 20 years -

Expected annual return: 12% -

Total invested: ₹36 lakh -

Estimated Return: ₹1.14 crore -

Projected corpus: ₹1.49 crore

In this example, we are ignoring exit loads, expense ratios, and taxes.

The numbers reveal a stark reality: waiting reduces your final corpus by nearly ₹3.8 crore, despite investing ₹18 lakh less. To match Priya’s ₹5 crore goal in just 20 years, Amit would need to invest approximately ₹70,000 monthly.

Your Path Forward

Starting early gives your money more time to grow exponentially. Even modest monthly investments can build significant wealth when given enough time.

How much should I invest monthly to reach ₹5 crore by retirement?

If you start at 30 with 30 years until retirement, you need approximately ₹15,000 monthly SIP assuming 12% annual returns. Starting at 40 requires roughly ₹70,000 monthly for the same goal.

Why does starting at 30 create ₹3.8 crore more than starting at 40?

Compound interest works exponentially over time. The extra 10 years allows your money to grow and reinvest returns multiple times, creating significantly larger wealth despite investing only ₹18 lakh more.

Can I start SIP with a small amount if I’m 30?

Yes, you can start SIPs with as little as ₹500 monthly. Starting small is better than delaying investment. You can increase the amount as your income grows.

What if I’m already 40? Should I still invest?

Absolutely. While starting earlier is advantageous, investing at 40 still gives you 20+ years for wealth creation. Focus on increasing your monthly contribution and maintaining consistency.

Are equity mutual funds safe for long-term retirement planning?

Equity mutual funds carry market risks but historically perform well over 15-20+ year periods. Professional fund managers handle portfolio allocation, making them suitable for long-term goals.

How do I calculate my retirement corpus requirement?

Consider your current expenses, inflation (typically 6-7%), desired lifestyle, and life expectancy. A general rule suggests 25-30 times your annual expenses at retirement.

If you start at 30 with 30 years until retirement, you need approximately ₹15,000 monthly SIP assuming 12% annual returns. Starting at 40 requires roughly ₹70,000 monthly for the same goal.

Compound interest works exponentially over time. The extra 10 years allows your money to grow and reinvest returns multiple times, creating significantly larger wealth despite investing only ₹18 lakh more.

Yes, you can start SIPs with as little as ₹500 monthly. Starting small is better than delaying investment. You can increase the amount as your income grows.

Absolutely. While starting earlier is advantageous, investing at 40 still gives you 20+ years for wealth creation. Focus on increasing your monthly contribution and maintaining consistency.

Equity mutual funds carry market risks but historically perform well over 15-20+ year periods. Professional fund managers handle portfolio allocation, making them suitable for long-term goals.

Consider your current expenses, inflation (typically 6-7%), desired lifestyle, and life expectancy. A general rule suggests 25-30 times your annual expenses at retirement.

Disclaimer: Mutual fund investments are subject to market risks, read all scheme related documents carefully. Past performance doesn’t guarantee future returns. Consult a certified financial advisor before making investment decisions.